Tax Systems Explained: Progressivity, Flat Rates, and History

When looking closely at a progressive vs flat tax model, evaluating how modern governments raise money reveals contrasting foundational economic theories.

1. Introduction: The Purpose of Taxation

At its core, taxation is the mechanism by which a government raises revenue to fund public goods and services. These range from physical infrastructure (roads, bridges) to social safety nets (unemployment benefits, healthcare) and national defense. You can explore other governance mechanisms in our foundational modules on the VoteView Courses Dashboard.

However, while the goal of raising revenue is universal, the method of collection varies. The two dominant models in modern democracies are the Progressive Tax System and the Flat Tax System. Weighing the structural benefits of a progressive vs flat tax approach involves analyzing baseline financial fairness and total economic efficiency.

🔑 Key Terms to Know

- Progressive Tax: A system where the tax rate increases as the taxable amount increases.

- Marginal Tax Rate: The tax rate paid on the last dollar earned. (Crucial: Earning more doesn’t mean all your income is taxed at the higher rate).

- Flat Tax: A proposal to replace multiple brackets with a single tax rate for everyone.

- Laffer Curve: An economic theory suggesting that there is an optimal tax rate that maximizes revenue; rates too high can discourage work and reduce total revenue.

- Vertical Equity: The principle that those with a greater ability to pay should contribute a larger percentage.

2. The Progressive Tax System (The Status Quo)

Today, the United States currently operates on a progressive income tax system. This model is based on the principle of vertical equity: the idea that those with a greater ability to pay should contribute a larger percentage of their income. Historically, the progressive vs flat tax debate centers on whether tracking income brackets remains fairer than uniform taxation layout rules.

How It Works

Income is divided into “brackets.” As a person earns more, only the income within the higher bracket is taxed at the higher rate.

Example: In the U.S., the first $11,600 of income might be taxed at 10%, while income above $578,000 is taxed at 37%.

Deductions & Credits: The U.S. system is unique for its complexity. Beyond brackets, it utilizes deductions (expenses subtracted from income) and credits (dollars subtracted directly from tax owed). These were originally designed to encourage specific behaviors (e.g., buying a home, having children) but have evolved into a complex web of loopholes. Learn more about macroeconomic behavior adjustments via the National Bureau of Economic Research (NBER) public database.

Historical Context

The Revenue Act of 1913 establishes the federal income tax following the ratification of the 16th Amendment.

The top marginal tax rate reaches an all-time high of 94% during World War II to fund the massive war effort.

Under President Reagan, top rates are significantly reduced from 70% down to 28%, sparking the modern debate on supply-side economics.

The system operates with 7 distinct brackets ranging from 10% to 37%, layered with numerous deductions and credits.

3. The Progressive vs Flat Tax Debate

By contrast, the Flat Tax is a theoretical alternative that proposes replacing the complex bracket system with a single tax rate applied to all taxpayers, regardless of income level.

How a Flat Tax Would Work

The Theory: Proponents argue that a flat tax simplifies the code, eliminates loopholes, and stimulates economic growth. This contrasts heavily with complex progressive models.

The Laffer Curve: Advocates argue that current high marginal rates discourage work and investment. Lowering the rate to a flat percentage (e.g., 15% or 20%) would expand the economy and potentially increase total revenue.

Arguments Against a Flat Tax

The Critique: Critics argue that a flat tax violates vertical equity. Because a fixed percentage takes a larger bite out of a low-income earner’s disposable income (money needed for survival) than a high-income earner’s, a flat tax is often described as regressive in effect. Evaluated contextually, the core arguments surrounding a progressive vs flat tax structure reflect completely opposite social safety priorities.

📊 Try It Yourself: Progressive vs Flat Tax Calculator

Interactive Tax Structure Calculator

Adjust the annual salary to observe how a Progressive Bracket System divides and taxes income compared to a 15% Flat Tax.

Progressive System (U.S. Model)

Bracket Tax Breakdown:

Flat Tax Proposal (15% Rate)

Bracket Tax Breakdown:

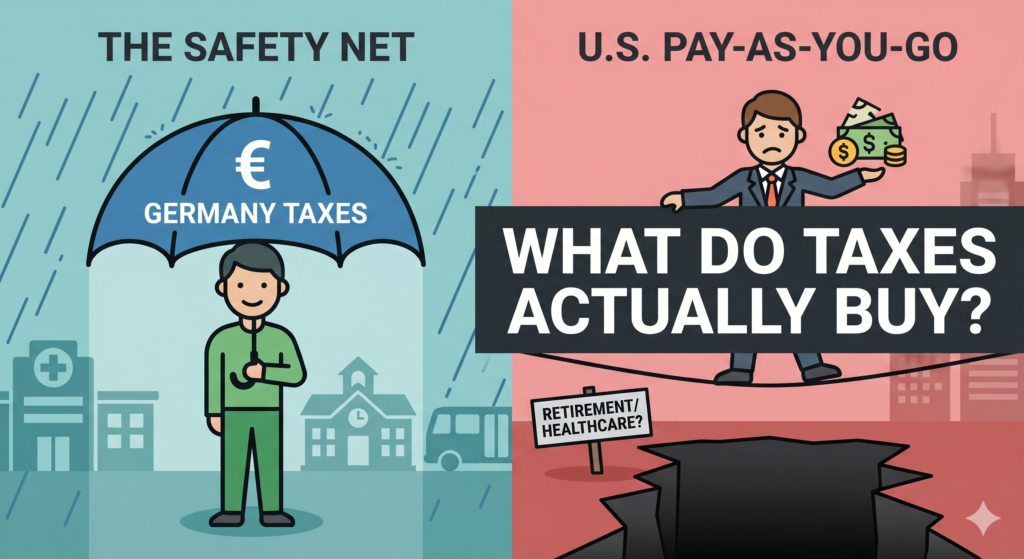

4. Comparative Case Study: The U.S. vs. Germany

To understand how these theories play out in reality, political scientists often compare the U.S. model with Germany’s highly progressive system.

| Feature | United States | Germany |

|---|---|---|

| Primary Philosophy | Individual Responsibility: Lower taxes, but citizens bear more of the direct cost for private needs. | Collective Security: Higher taxes fund a comprehensive, state-managed safety net. |

| Tax Structure | Progressive: 7 Federal Brackets (10% to 37%). | Highly Progressive: Rates climb to 42% (and 45% for top earners). |

| Complexity | High: Extensive deductions, credits, and itemized filing paths. | Moderate: Fewer loopholes; highly standardized social contributions. |

| Revenue Allocation | Mixed: Funds infrastructure, national defense, and limited social programs. | Comprehensive: Funds universal healthcare, free public university, and robust unemployment safety nets. |

5. The Economic Debate: Progressive vs Flat Tax Priorities

The debate over tax systems ultimately boils down to a trade-off between two major economic goals:

Efficiency (Pro-Flat Tax): Complex tax codes create “deadweight loss”—resources wasted on tax preparation, legal maneuvering, and avoidance strategies rather than productive work. The goal is to maximize economic output by simplifying the code and rewarding extra effort.

Equity (Pro-Progressive): A fair society requires a degree of wealth redistribution to ensure a baseline standard of living for all citizens. The goal is to reduce extreme inequality and fund essential public goods that the private market cannot provide efficiently or fairly.

6. Conclusion: No Perfect System

There is no mathematical formula that determines the “correct” tax rate. Every system involves a fundamental trade-off:

- The U.S. system prioritizes individual retention of capital but accepts higher private costs and inequality.

- The German system prioritizes collective security and equality but requires higher upfront contributions from its citizens.

- The Flat Tax promises simplicity and growth but risks reducing revenue and increasing the burden on lower-income earners.

Understanding these mechanics is the first step in evaluating tax policy. It moves the classroom conversation away from a simple “taxes are bad” narrative and toward a more meaningful question: “What kind of society do we want to fund?”

Reading Check: Tax Systems Quiz

Test your understanding of progressive vs. flat taxes, marginal rates, and the U.S. vs. Germany case study.

1. According to the text, what does a progressive tax system mean for taxpayers as their income increases?

2. Which of the following best defines the concept of a ‘Marginal Tax Rate’ as emphasized in the text?

3. During which historical event did the top marginal U.S. federal income tax rate reach its peak of 94%?

4. Critics argue that a Flat Tax is often ‘regressive’ in effect because:

5. Based on the case study comparing the U.S. and Germany, which statement accurately reflects Germany’s model?